Profit Participation Rights for Employee Participation in Start-ups – A Real Alternative to VSOPs?

I. Introduction

Incentivizing employees plays a crucial role, especially in start-ups. With the new regulation of Sec. 19a EStG (German Income Tax Act), which came into force on January 1, 2024, the legislator added a practical tool to the range of employee participation forms alongside VSOPs (Virtual Share Option Programs), ESOPs (Employee Share Option Programs), Hurdle Shares, etc. However, in practice, participation under Sec. 19a EStG is primarily considered for the (additional) participation of founders and C-level management members rather than for the participation of (a large number of) employees. The main reason for this is the higher effort involved (consideration in the shareholders’ agreement, notarial certification requirements, obtaining a wage tax ruling) compared to VSOPs. Currently, in practice, VSOPs are still seen as the most common employee participation model for (a large number of) employees, with the following points usually speaking in favor of VSOPs from the start-up's perspective:

- Granting only requires the conclusion of a contractual agreement between the beneficiary and the company. No notarial certification requirements exist.

- Virtual options generally do not grant shareholder rights, particularly no participation or voting rights in shareholders’ meetings.

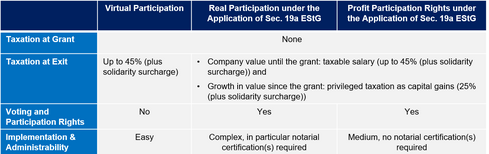

However, VSOPs have a significant disadvantage: for the beneficiaries, the payment of the profit participation in the event of an exit is a type of bonus payment, leading to fully taxable (wage) income. Taxation occurs only at the time of payout (avoiding the so-called dry income issue), usually in the event of an exit. However, the payout amount is fully taxable at the beneficiary's personal tax rate, which can be up to 45 % (plus solidarity surcharge). Thus, the tax disadvantage of virtual participation models compared to real participation models is evident: in the case of a real participation, the beneficiary enjoys the privileged taxation of the profits realized upon an exit as capital income, usually taxed at the flat rate of 25 % (plus solidarity surcharge).

II. Tax Deferral through Application of Sec. 19a EStG

Sec. 19a para. 1 EStG can be applied if the start-up (the employer) has not exceeded the following thresholds at the time of granting the capital participation or in any of the six preceding calendar years:

Furthermore, the start-up must not be older than 20 years.

Employees can be granted real participation by the employer or a shareholder of the employer free of charge or at a reduced price according to Sec. 19a EStG (i. e., the employee can either acquire new shares in the context of a capital increase or the employer or a shareholder of the employer can transfer existing (own) shares to the employee) without triggering dry income taxation.

Although the granting of the shares to the employee still results in a taxable benefit in kind, this does not lead to taxation in the calendar year of the grant according to Sec. 19a para. 1 EStG. Instead, taxation is deferred. Pursuant to Sec. 19a para. 4 EStG the untaxed benefit in kind is subject to taxation according to Sec. 19 EStG and wage tax deduction as other income only when:

- The capital participation is transferred in whole or in part, with or without consideration;

- 15 years have passed since the transfer of the capital participation, or

- The employment relationship with the employer ends.

How nice would it be if one could combine the advantages of virtual and real participation models under the application of Sec. 19a EStG – the best of both worlds, so to speak? And this is where profit participation rights (PPRs) come into play. From a tax perspective, profit participation rights are attractive because, like a real shareholding, they lead to capital gains, i. e. repayments and capital gains are generally subject to taxation at the flat rate of 25 % (plus the solidarity surcharge).

Sec. 19a of EStG applies to “capital participations within the meaning of Sec. 2 para. 1 no. 1 lit. a, b and f to l and (2) to (5) of the Fifth German Capital Formation Act” (5. VermBG) and, in addition to real shares, these may also include profit participation rights.

III. What are Profit Participation Rights?

Profit participation rights are not legally regulated, but their existence is assumed in various legal regulations, such as the Stock Corporation Act (Sec. 221 para. 3 and 4 AktG), the Transformation Act (Sec. 23 UmwG), or the Fifth Capital Formation Act (Sec. 2 para. 1 no. 1 lit. l 5. VermBG). Profit participation rights are contractual creditor rights that are essentially similar to rights typically held by shareholders of a GmbH, without, however, conveying shareholder participation rights. Profit participation rights can be designed in various ways.

The classic understanding of profit participation rights for employee participation is as follows: In an employee profit participation right, the employee provides the employer with capital for a certain period. In return, the employee receives a share in the employer's entrepreneurial success. At the end of the profit participation right's term, the employee is entitled to the return of the provided capital, provided no loss participation has been agreed upon. This classic understanding is difficult to reconcile with employee participation in start-ups. This is because, in start-up employee participation, it is not desired for the employee to actually provide capital to the start-up. On the contrary, employee participation is usually intended to compensate for the lower salaries in the start-up sector compared to established companies. Furthermore, no return of this capital at the end of the term is desired, but rather participation in the proceeds in the event of an exit. However, upon further consideration, it becomes clear that if one moves away from the classic understanding and considers the essential requirements for the existence of profit participation rights, their use for employee participation in start-ups is indeed conceivable.

IV. Profit Participation Rights in Start-ups and Sec. 19a EStG

Since the aim of granting profit participation rights in the start-up sector is to find a tax-attractive alternative to VSOPs, the goal must be to fall within the scope of Sec. 19a EStG. Only then can the dry income issue be avoided. To achieve this goal, the conditions provided for profit participation rights in the 5. VermBG must be met, i. e.:

- The profit participation right must be associated with a right to the company's profit,

- The beneficiary must not obtain the status of a co-entrepreneur within the meaning of Sec. 15 para. 1 no. 2 EStG, and

- No repayment of the profit participation right at nominal value must be provided.

These key points must be considered despite the flexibility in designing the profit participation right conditions. If successful and thus Sec. 19a EStG applies, the tax effects are as follows:

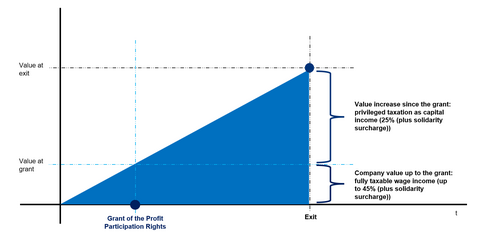

- Company value up to the grant: fully taxable wage income (up to 45 % (plus solidarity surcharge)), and

- Value increase since the grant: privileged taxation as capital income (25 % (plus solidarity surcharge)).

Currently, there is no "blueprint" for granting profit participation rights under the application of Sec. 19a EStG. If one decides to implement an employee participation program based on profit participation rights, it is advisable (currently) to coordinate the application of Sec. 19a EStG with the responsible tax office through a (free) wage tax ruling (Sec. 42e EStG).

V. Terms of Profit Participation Rights

A comparison of the main regulations of profit participation rights and VSOPs shows that it is possible to design profit participation rights falling under Sec. 19a EStG similar to a VSOP. Below, we point out the (many) similarities and (few) differences.

1. Contract Drafting and Formal Requirements

Granting a virtual option only requires the conclusion of a contractual agreement between the beneficiary and the start-up. No notarial certification requirements exist. Typically, VSOPs are set up whose conditions generally apply to all beneficiaries. The grant is then made through separate letters to the individual beneficiaries, which generally allow for individual conditions to be set or modified.

There is also extensive contractual freedom in the individual draft of profit participation right conditions. Here, too, there are no notarial certification requirements, nor is there anything against drafting the profit participation right conditions as a program with individualized grant letters.

If the profit participation right conditions are standardized, they are subject to the AGB control according to Sec. 307 et seqq. BGB (German Civil Code), just like VSOPs.

2. Beneficiaries

VSOPs often intend that virtual options can be granted not only to employees of the start-up but also to consultants, freelancers, members of the advisory board, etc. The grant of profit participation rights under the application of Sec. 19a EStG, on the other hand, is only possible for employees of the start-up. The tax deferral under Sec. 19a EStG is not available for consultants, freelancers, members of the advisory board, etc. Also, the grant cannot be made to a holding company of the employee, which usually makes less sense for a VSOP due to the lack of tax advantages.

Currently, the tax deferral under Sec. 19a EStG is only possible if the participation concerns the employer's company. With the Annual Tax Act 2024, which the Bundestag approved on October 18, 2024, and which is on the agenda in the Bundesrat on November 22, 2024, a significant new regulation is planned with the introduction of a so-called group clause. This will allow participation in another group company to be favored in the future, so that profit participation rights, like virtual options, can be granted, for example, in the parent company of the employing company.

3. Equalization with Common Shares

In VSOPs, beneficiaries are granted a certain number of virtual options. Typically, one virtual option corresponds to a non-preferred common share with a nominal value of EUR 1.00 (sometimes a different conversion factor is chosen though) and is thus economically equivalent to the common shares held by the founders. This can also be achieved with the issuance of profit participation rights. Profit participation rights can generally be issued at any nominal value. This allows for equalization with non-preferred common shares with a nominal value of EUR 1.00 by granting the profit participation right holders a capital participation as if they held a corresponding number of such common shares according to the profit participation right conditions.

4. Discounted Issuance/Base Price/Profit Participation Right Capital

No consideration is required at the time of granting virtual options. VSOPs usually provide for a so-called base price (also called strike price). In the early stages of the start-up, this usually amounts to EUR 1.00 (corresponding to the nominal value per share). In a later phase of the start-up, a base price above EUR 1.00 per virtual option is usually agreed upon. The base price often depends on the pre- or post-money valuation of the last financing round before the virtual options are granted. All participation models aim to allow the beneficiaries to participate in the start-up's value increases to which the beneficiaries (employees) have contributed through their work. This is reflected in VSOPs through the base price. However, the base price is not to be paid by the beneficiary but is deducted from their profit participation in the event of an exit.

This is different when granting profit participation rights. Profit participation rights have – similar to real shareholding – a financing function, so the beneficiaries must pay at least a certain, albeit small, amount to the company. Until today there is no consensus on how high this amount should be. In our opinion, an amount based on the share capital should be sufficient.

The difference between the amount paid by the beneficiary and the actual value of the profit participation rights at the time of granting then represents a monetary benefit, which would generally be taxable as part of the wage income at the time of granting, similar to a discounted grant of real shares. However, due to the tax deferral of Sec. 19a EStG, the dry income issue does not arise.

After granting the profit participation rights, the start-up should confirm the untaxed monetary benefit with the responsible tax office through a free wage tax ruling (Sec. 42e EStG). Confirming the amount of the untaxed benefit requires that both the determined value and the documents for the valuation are submitted to the tax office, usually by the employer. The task of the tax office is to review, not to determine the value to be confirmed.

It should be noted that the monetary benefit must be determined for each grant of profit participation rights. The valuation of a financing round or a secondary can only be used if it is less than 12 months old (see Sec. 11 para. 2 BewG (German Valuation Law)). Otherwise, obtaining a valuation report or, under certain circumstances, a valuation according to the simplified income value method may be considered (see Sec. 11 para. 2 BewG). This will regularly lead to profit participation rights being granted only at certain intervals, considering the then applicable valuation, unlike virtual options.

5. Participation in Exit Proceeds

Virtual options grant the beneficiaries a contractual claim to the exit proceeds, with the beneficiaries being economically equated to holders of non-preferred common shares in the start-up when distributing the exit proceeds.

Profit participation rights can, among other things, convey participation in the so-called liquidation proceeds and the associated hidden reserves. For employee participation in the start-up sector, a profit participation right can also provide for a capital participation of the beneficiary in the event of an exit, as if they were involved with a certain number of non-preferred common shares in the start-up.

The profit participation right is then terminated or possibly sold. In addition to the paid profit participation right capital, the beneficiary then receives compensation based on a hypothetical participation in the issuing company. As a result, the beneficiaries participate in the company's value increase realized through the exit proceeds, just like in the case of a VSOP.

6. Participation in Profits

VSOPs rarely provide for the beneficiaries' participation in any profit distributions.

However, to apply Sec. 19a EStG to profit participation rights, they must be associated with a "right to profit" as derived from Sec. 2 para. 4 of the 5. VermBG. Therefore, the profit participation right conditions must necessarily provide for participation in ongoing profits. Due to the lack of foreseeable profits, this criterion is initially irrelevant for most start-ups. However, it should not be overlooked that profits can be achieved before an exit. Therefore, the profit participation right conditions should anticipate under what circumstances such claims arise, suggesting a synchronization with actual distributions, similar to a VSOP with participation in ongoing profits.

The Federal Ministry of Finance provides important guidance in its decree dated April 11, 2023, on the income tax treatment of profit participation rights, under which conditions this requirement is considered fulfilled.

7. Vesting

VSOPs typically include so-called vesting provisions. Vesting provisions are designed to bind beneficiaries to the start-up and incentivize their commitment and loyalty to the company by stipulating the partial or complete forfeiture of virtual options if a beneficiary has not worked for the start-up for a certain minimum period or has committed a serious breach of duty, for example.

Such vesting provisions can also be reflected in the terms of profit participation rights. Unlike a VSOP and similar to a real shareholding, in the case of a bad leaver, at least the capital contributed for the profit participation rights (taking into account any loss participation) must be repaid.

In the event of a repurchase of the profit participation right by the employer, a shareholder of the employer, or a company within the meaning of Sec. 18 AktG, the fair market value is replaced for tax purposes by the compensation granted by the employer, a shareholder of the employer, or a company within the meaning of Sec. 18 AktG (Sec. 19a para. 4 sentence 4 2nd half-sentence EStG), so that adverse tax consequences for the employee can be avoided.

Furthermore, specific provisions must be made to comply with the requirements of Sec. 19a EStG. For profit participation rights that remain with the beneficiary in the event of termination of the service or employment relationship - in accordance with the vesting rules -, it is advisable, for example, to provide that the start-up (the employer) declares to the tax authorities that it is liable for the (wage) tax to be withheld and paid. This is because only then can the taxation be deferred despite the termination of the employment relationship (cf. Sec. 19a para. 4a EStG). This declaration by the employer can thus be seen as the core of the new regulation of Sec. 19a EStG to avoid the dry income issue.

8. No Shareholder Rights

Virtual options generally do not grant shareholder rights, particularly no participation or voting rights in shareholder meetings.

Profit participation rights, even though they can be flexibly structured, do not grant shareholder rights either, particularly no participation or voting rights in shareholder meetings. Certain information rights can be provided. However, rights that arise from a shareholder's membership position cannot be granted with profit participation rights, otherwise, the beneficiary could develop a harmful co-entrepreneurial initiative, leading to the assumption of a co-entrepreneurship and thus the non-applicability of Sec. 19a EStG.

As stated above, according to the 5. VermBG, profit participation rights must not be associated with a co-entrepreneurship within the meaning of Sec. 15 para. 1 sentence 1 no. 2 EStG. For co-entrepreneurship, it is crucial that the beneficiary bears the so-called co-entrepreneurial risk and can develop a so-called co-entrepreneurial initiative, with both conditions generally having to be met cumulatively for co-entrepreneurship to be affirmed.

The co-entrepreneurial initiative usually lies in the exercise of voting, control, and objection rights. If the beneficiary is not granted any such rights, they cannot develop a co-entrepreneurial initiative. Thus, profit participation rights would not be associated with co-entrepreneurship. Therefore, it is important to ensure that the terms of the profit participation rights do not grant the beneficiaries any rights that could lead to the assumption of a co-entrepreneurial initiative. The granting of mere information rights is generally harmless.

9. Dilution

VSOPs generally do not provide for anti-dilution protection. Therefore, virtual options are economically diluted in the event of future capital increases in the start-up's share capital. The only exception is a capital increase from company funds, where the number of virtual options increases in the same proportion as the share capital after the capital increase.

This principle applies correspondingly to profit participation rights. However, any anti-dilution protection can, of course, be contractually agreed upon for both virtual options and profit participation rights.

10. Transferability Exclusion

The transfer of profit participation rights to third parties should generally be excluded in the terms of the profit participation rights, as is usually the case with VSOPs. This is also possible because a benefit from the discounted transfer of capital participations within the meaning of Sec. 19a para. 1 sentence 1 EStG is considered to have been received for wage tax purposes even if it is legally impossible for the employee to dispose of the equity participation (Sec. 19a para. 1 sentence 3 EStG, cf. BMF letter of June 1, 2024 (Wage tax treatment of the provision or transfer of equity participations from 2024 (Sec. 3 no. 39, Sec. 19a EStG)), marginal number 35.2).

11. Consent Requirements

For VSOPs, at least a consenting resolution of the shareholders' meeting is obtained during the implementation of the VSOP. Usually, the consent is already given in connection with a financing round, so the VSOP is part of the contractual documentation (usually the shareholders' agreement), which also regulates the maximum number of virtual options to be granted and any consent requirements for the individual granting to specific beneficiaries.

If profit participation rights also include participation rights in profits and liquidation proceeds, this affects the shareholders' capital rights. Therefore, a shareholders' resolution with a majority amending the articles of association analogous to Sec. 221 para. 1 AktG should be passed before issuing such profit participation rights. Whether shareholders have a subscription right analogous to Sec. 221 para. 4 AktG is disputed. However, it is advisable, as is customary with VSOPs, to regulate the framework for granting profit participation rights in a shareholders' agreement, combined with a waiver of subscription rights.

In summary, it can be stated that, apart from a few specific features to be considered when designing the terms of profit participation rights, these can generally be structured very similarly to VSOPs.

VI. (Tax) Accounting Treatment by the Employer

The Federal Ministry of Finance commented on the income tax treatment of profit participation rights in its decree dated April 11, 2023. However, the decree is widely criticized and leaves some questions unanswered. Based on such letter, the profit participation rights issued as part of an employee participation scheme in accordance with the above principles should be recognized as debt in the employer's tax balance sheet. The initial recognition should then be at the fair market value of the issued profit participation right and represent a tax-deductible wage expense in the amount of the monetary benefit (i. e., deducting the capital contributed for the profit participation right by the employee). When drafting the profit participation rights, it should be noted that recognition is excluded if the profit participation right does not yet represent an economic burden for the employer company. To avoid adverse tax effects on the employer, this should not be overlooked when designing the terms of the profit participation right.

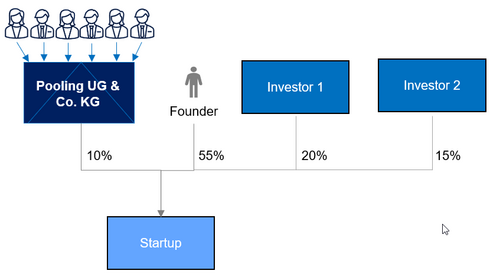

VII. Comparison to the Pooling-KG Variant

In practice, the application of Sec. 19a EStG is sometimes combined with the Pooling-KG model. The beneficiaries are then not directly involved in the start-up but pooled through a Pooling-KG, which in turn holds an actual participation in the start-up.

Both the profit participation rights and the Pooling-KG variant (combined with an actual participation) have advantages and disadvantages that need to be weighed and discussed to find the optimal solution for the individual case. The Pooling-KG model generally corresponds more closely to the legal concept and can be seen as a common structure for management and employee participation. However, the complexity of the limited partnership agreement of the KG should not be underestimated. Additionally, there are ongoing costs (annual financial statements, tax returns, further administration) and some legal and tax pitfalls to consider (vesting provisions, cost bearing, holding own shares, etc.). Particularly, in the case of a Pooling-KG variant, coordination with the tax authorities may be advisable.

VIII. Conclusion and Outlook

Profit participation rights offer a flexible and easy-to-administer option for employee participation. It is not yet clear whether profit participation rights or the Pooling-KG variant will be the better model for employee participation in the long term.

Whether employee participation using profit participation rights in conjunction with the application of Sec. 19a EStG can establish itself in the start-up scene will depend, in particular, on how the tax authorities handle this instrument in connection with Sec. 19a EStG.

In our opinion, it is advisable to seek coordination with the tax authorities before the initial issuance of profit participation rights by obtaining a wage tax ruling to ensure that the profit participation rights to be granted actually fall within the scope of Sec. 19a EStG. Another wage tax ruling should then be obtained after the grant to confirm the valuation of the monetary benefit granted with the issuance of the profit participation rights. These necessary coordination, lead to higher effort compared to the granting of virtual options and should also be considered in the timeline.

Furthermore, it remains to be seen how foreign employees and investors will deal with this, as profit participation rights are relatively unknown internationally and may be a less attractive model for employees residing abroad.

In any event, when structuring employee participation programs, profit participation rights should always be considered since the amendment of Sec. 19a EStG.