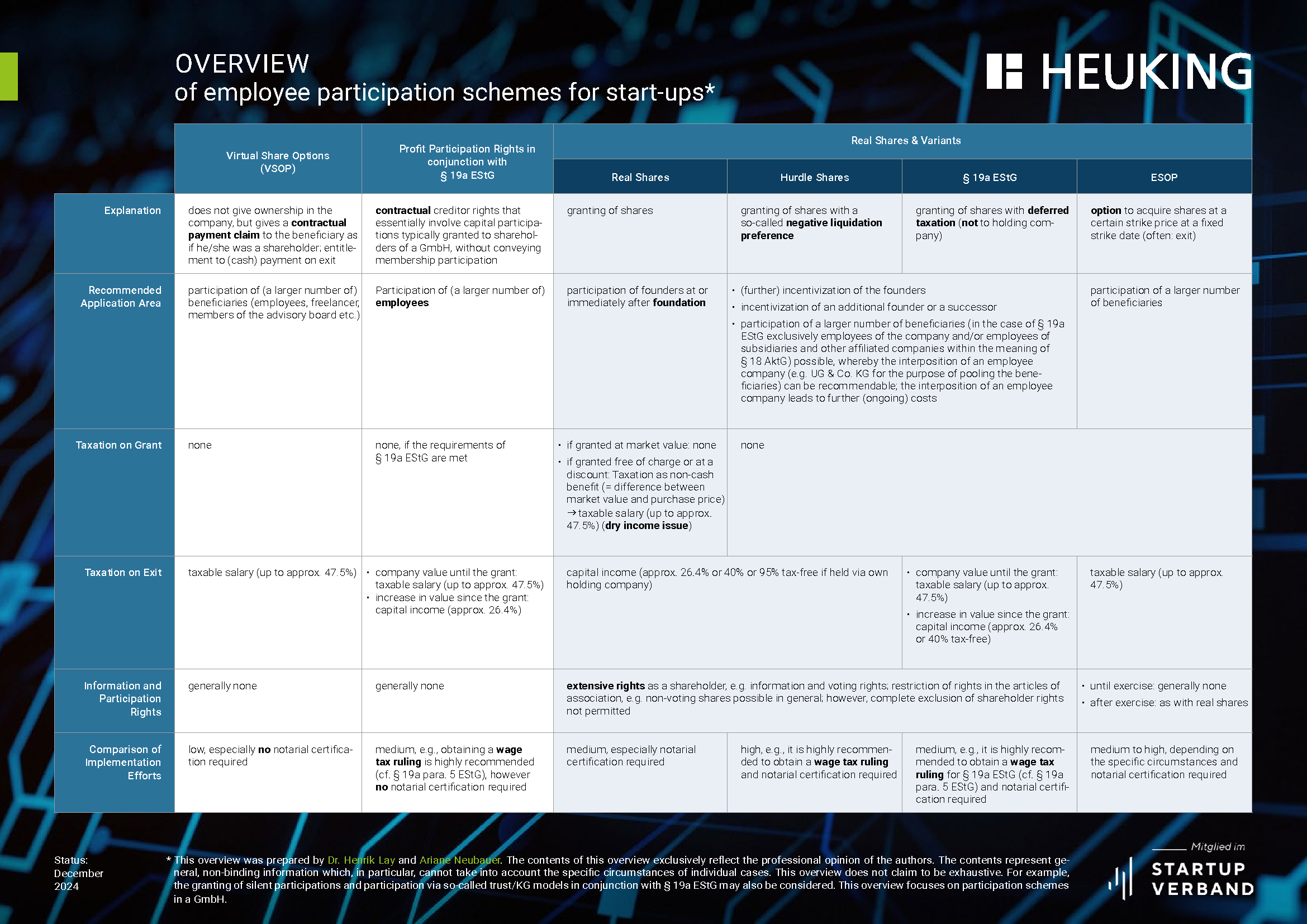

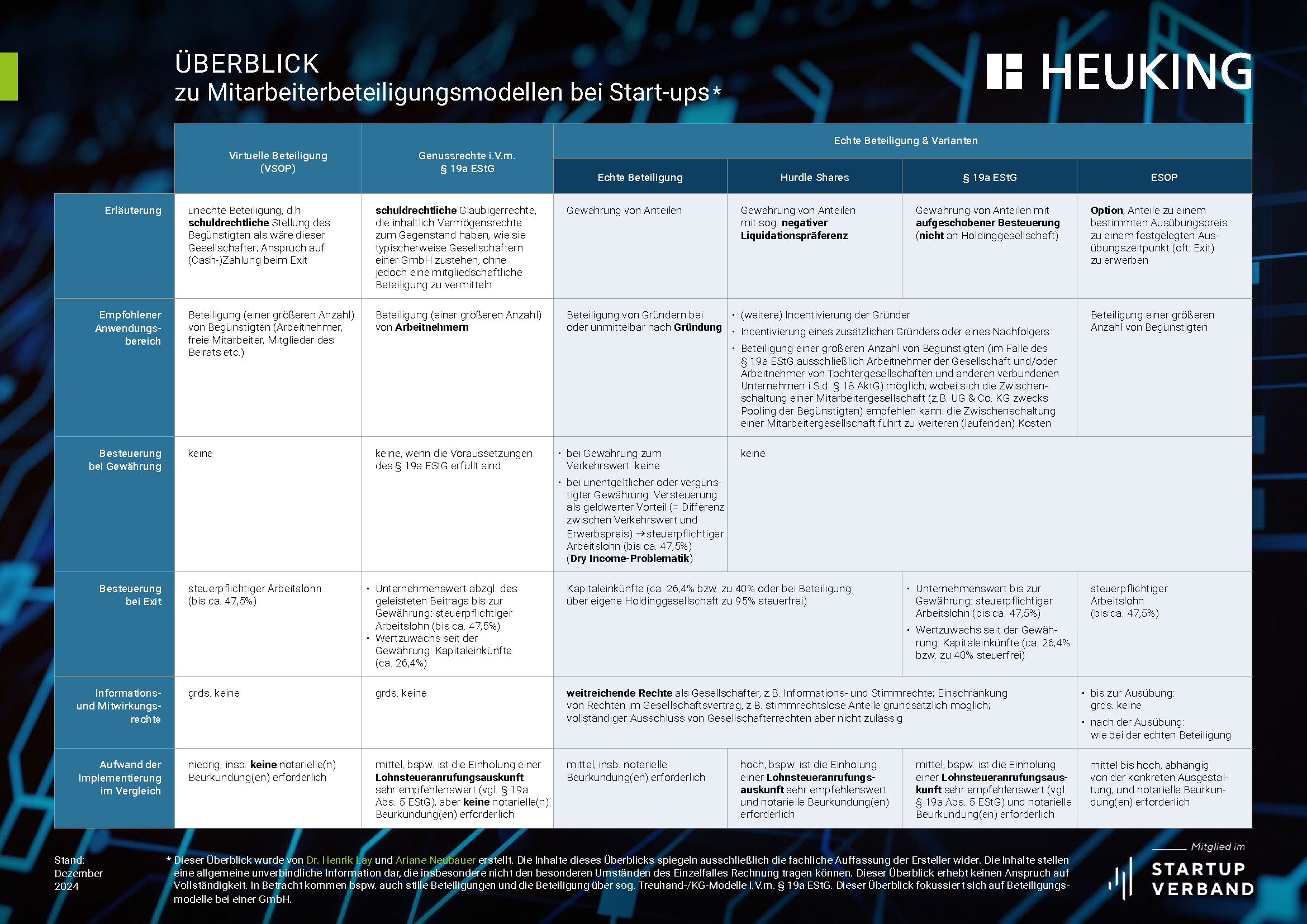

Updated Overview of Employee Participation Schemes for Start-ups

The updated overview of employee participation schemes for start-ups provides a comprehensive summary of the various models of employee participation for start-ups, including the latest legal changes and an addition for profit participation rights in connection with § 19a EStG.

Important Innovations and Additions:

- Implementation of the Group Clause: The implementation of the so-called group clause in § 19a EStG now allows employees of subsidiaries and other affiliated companies within the meaning of § 18 AktG to benefit from the tax deferral according to § 19a EStG when granting shares in start-ups. Specifically, the tax deferral can now also be claimed for shares in companies within a group, provided that the group as a whole meets the thresholds according to § 19a para. 3 EStG and none of the group companies are older than 20 years. The group clause is particularly important for foreign start-ups with subsidiaries in Germany.

- Profit Participation Rights in conjunction with § 19a EStG: The overview has now also been expanded to include profit participation rights in conjunction with § 19a EStG. This form of employee participation can be an attractive alternative to the classic virtual participation models (VSOP). We discuss this model in detail in our article from 07.11.2024 (Profit Participation Rights for Employee Participation in Start-ups – A Real Alternative to VSOPs?).